Single-Payer Healthcare Isn’t the Answer — Standardization Is

tl;dr: Our healthcare system’s incentives are broken. To fix it, we must inject transparency through standardized health insurance contracts and an independent clearinghouse to handle claims, provider pricing, and coverage consistently.

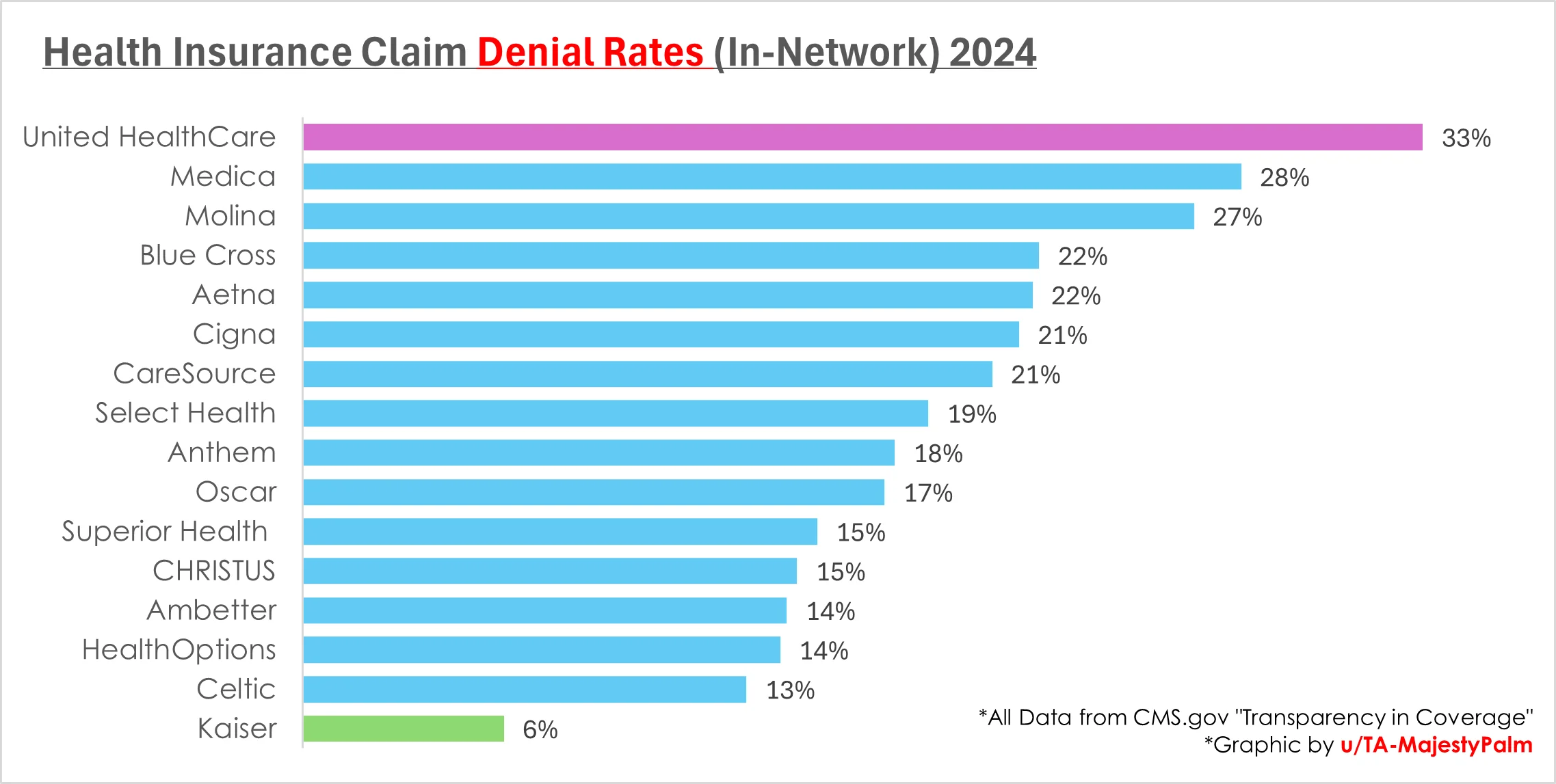

I spent this past summer neck-deep in the health insurance world. I’ve talked to consumers reeling from bewildering bills, doctors drained by paperwork and overhead, hospital executives juggling razor-thin margins, and CEOs of both startups and giant insurers who admit the system is on shaky foundations. In the U.S., health insurance often feels like a labyrinth, where each player points fingers at someone else. Patients blame insurers for denials and complexity. Insurers point to hospitals for charging too much. Hospitals fault drug prices and physician demands, and doctors say they’re hamstrung by insurers and malpractice pressures. It’s a maddening cycle of blame, where no one emerges clean—and patients suffer most.

This tension recently boiled over in a horrific way. An assassin shot Brian Thompson, the CEO of UnitedHealthcare's insurance arm, reportedly protesting “delay, deny, defend” tactics. This act of violence is indefensible. Yet it painfully illustrates the desperation and anger simmering beneath the system’s surface. People are terrified that a claims denial could ruin them, and they see no transparency or fairness in the process. Lack of transparency has consequences, and we’re witnessing them in the darkest form.

Why Is This Happening?

Today’s health insurance market feels like a tangle of contracts—secretive, custom deals with little shared ground. Other markets used to look like this too. Decades ago, commodity trading was a mess until standardized futures contracts brought clarity. By agreeing on specifications, delivery points, and quality standards, these markets became transparent and competitive. Everyone understood the rules, and price discovery was fair.

Health insurance hasn’t undergone that transformation. Yes, we have the ACA’s “metal tiers” (Bronze, Silver, Gold, Platinum), but these categories remain vague. One Silver plan can differ drastically from another in coverage details, networks, and hidden exceptions. Patients picking plans often rely on guesswork and luck, rather than clear comparisons.

A Path to Transparency: Standardized Contracts and a Clearinghouse

What if we took a cue from futures markets and standardized health insurance at its core? We could refine the ACA tiers so that “Silver” means the same thing no matter which insurer you choose. Every Silver plan would have identical cost-sharing, identical rules for common treatments, and a uniform approach to hospital and specialist access. Consumers could finally compare like with like.

The next step is to create an independent clearinghouse for claims and provider pricing. Hospitals and clinics that wish to participate must adopt a standardized fee schedule, openly accessible to all. Insurers then integrate with these transparent networks, processing claims under universal rules. This approach curbs the “delay, deny, defend” tactics, ensuring fairness. With a shared playbook, insurers compete on price, brand, customer experience, operational efficiency, and financial management—rather than relying on opaque coverage maneuvers. Providers benefit from consistent, predictable pricing, while patients gain clarity on what they’re actually purchasing.

What about Value-Based Care?

On paper, VBC sounds great. Instead of paying providers by volume (the more tests, the more money), we pay them by outcomes. Better care leads to better reimbursements, aligning incentives for quality over quantity.

But in practice, VBC has often disappointed. Why? Because it stacks yet another layer of complexity onto an already opaque system. Measuring “value” requires intricate metrics that can be gamed, debated, and adjusted. Without standardized, transparent pricing and coverage, “value” becomes just another variable tangled in the same Gordian knot of mistrust and confusion. Providers shuffle resources to improve reported metrics, insurers tweak their definitions of value, and patients still don’t get the straightforward, predictable coverage they deserve. Rather than simplifying the market, VBC can turn it into an even more complex puzzle—one that well-meaning initiatives struggle to solve.

In contrast, the clearinghouse/futures model aims first for transparency and fairness. It sets the table with clear rules and prices, removing the hidden profit corners and secret deals. Once you have a stable, visible baseline, you can layer on targeted incentives for better outcomes. But you need that transparent foundation first. Without it, VBC can feel like rearranging deck chairs on the Titanic—it’s a well intentioned attempt that doesn’t actually address the ship’s structural problems.

Taming the Circle of Blame

By creating standardized contracts and a clearinghouse, the circle of blame loses its hiding places. Patients no longer face indecipherable differences among plans. Insurers can’t point fingers at hospitals for outrageous demands when prices are public and uniform. Hospitals and doctors operate in a system where failing to provide good value is obvious and has consequences.

Implementation Details

The U.S. already has core components that can support a futures-like model. The ACA’s metal tiers (Bronze, Silver, Gold, Platinum) provide a foundation for standardized benefit packages, while the ACA marketplaces offer a structured platform for consumers to compare these plans. We also have existing medical clearing infrastructures—like those provided by Change Healthcare—that already facilitate the secure exchange of claims and payment data.

By leveraging the ACA’s tiers and marketplaces, and integrating established clearing systems, we can enforce standardized contracts, clarify pricing, and streamline risk adjustment and subsidies. Instead of building a new system from scratch, we refine what we have—transforming the current patchwork into a transparent, accessible market where new insurers, employers, and consumers can confidently engage.

Reining in Costs and Complexity

This approach, rooted in transparency, can help control soaring healthcare costs. If a certain service is overpriced, it will stand out. Competition—actual, visible, rules-based competition—replaces negotiations behind closed doors. Over time, the market pressure nudges everyone toward efficiency and fairness, something value-based care has struggled to achieve amid complexity and gaming.

A More Humane Market

We’re dealing with human lives, not bushels of wheat. But the principle applies: standardization and transparency prevent exploitation and confusion. Patients should know what they’re buying. Doctors should practice without armies of coders and admin staff. Insurers should focus on real innovation, not smoke-and-mirrors coverage variations. The futures-like model provides a stable groundwork on which humane, patient-centered policies can thrive.

It’s not too late.

The horrifying murder of Brian Thompson is a disturbing sign that our system can push people to despair. Brian Thompson & his murderer are both the victims of a system with broken incentives. We owe it to ourselves to try something different. By embracing standardized contracts and an independent clearinghouse, we clear the fog. We see the true costs and benefits. We find out who’s really adding value and who’s simply extracting rents. Once we have that baseline, then we can talk about truly rewarding high-quality care—without layers of complexity that no one can fully understand but we have to start with standardization of health insurance.